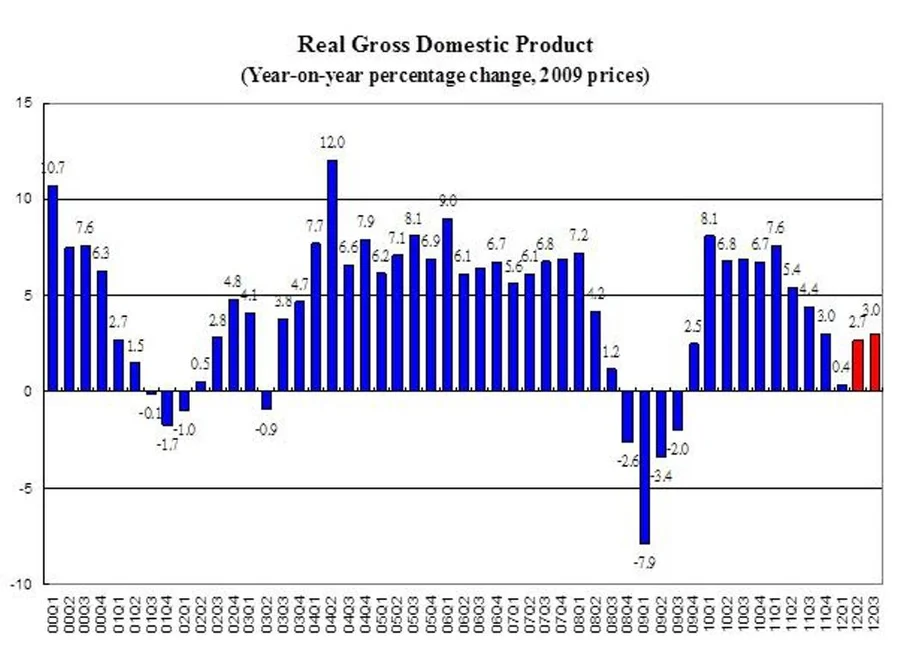

Professor Richard Wong Yue-Chim, Professor of Economics at HKU said that, "Weighed down by the crises in the Euro zone, slow economic recovery in the United States and deceleration of economic growth in the Mainland, Hong Kong's external demand has begun to slowdown since the second quarter of last year. The trade sector contracted in the first quarter, dragging real GDP growth to be only 0.4% in 12Q1. More accommodative monetary policies by central banks in the developed world, as well as in the Mainland, will provide support for continued expansion of the global economy. The GDP growth in the current quarter is roughly equally driven by domestic and external demand, with net external demand accounting for 1.4 percentage points of the overall 3.0% GDP growth, and domestic demand accounting for the rest."

"The labour market is projected to remain relatively stable with the unemployment rate projected to increase to 3.4% in 12Q3, up from 3.3% in 12Q2. The number of unemployed workers is forecast to rise by 5,000, and the number of employed workers is estimated to go up by 19,000 in the current quarter. Inflation pressure is ease further, with the price level, as measured by the composite CPI, estimated to increase by 4.7% in 12Q3," according to Dr. Alan Siu, Executive Director of the Hong Kong Institution of Economics and Business Strategy at HKU.

The forecast details are in Table 1 and Table 2, and the forecasts of selected monthly indicators are in Table 3. All growth rates reported are on a year-on-year basis.

Forecast Highlights

· Given a more uncertain economic outlook, private consumption spending grew by 5.6% in 12Q1, decelerating from the 6.6% growth in 11Q4. The deceleration in the growth of consumption spending will continue. Private consumption spending is projected to grow, but at a slower pace, with a growth rate forecast to be 3.8% in 12Q2 and decelerate to 3.3% in 12Q3.

· The volume of retail sales grew by 5.8% in May 2012, slower than the 7.6% in April 2012. The slowdown in visitor arrivals, as well as the sharp fall in spending on expensive items by visitors from the Mainland, will continue to put a drag on the growth of retail sales. The growth of the volume of retail sales is expected to moderate to 6.6% in 12Q2 and 5.6% in 12Q3.

· Dropping from the anemic 2.0% growth in 11Q4, total exports of goods dropped by 5.7% in 12Q1, reflecting the debt crisis in the Euro zone. External demand is projected to grow in the 2nd and 3rd quarters, supported by more accommodative policies of the major central banks. In May 2012, the exports of goods from Hong Kong grew by 5.6%, with electrical machinery, telecommunication equipment and office machinery rose by 0.9%, 32.0% and 26.2% respectively. The total exports of goods is estimated to grow by 1.8% in 12Q2, and is forecast to pick up to grow by 3.0% in the 12Q3.

· Imports of goods decreased by 2.7% in 12Q1, reverted from the 3.9% growth in 11Q4. In tandem with the rebound in the exports of goods, imports of goods also rose by 4.6% in May 2012, with telecommunication equipment and office machinery growing by 24.4% and 36.1% respectively. The growth of imports of goods is forecast to growth by 1.6 in 12Q2 and 2.6% in 12Q3.

· Service exports grew by 3.6% in 12Q1, decelerating from the 5.3% growth in 11Q4. Visitor arrivals moderated from 14.4% growth in April 2012 to 12.7% growth in May 2012. The pickup in visible trade will increase the demand for trade related services in 12Q3, offsetting the slowdown in visitor arrivals. The increase in service exports is forecast to be 2.9% in 12Q2 and picking up to 3.3% in 12Q3.

· Service imports went up by 2.5% in 12Q1, decelerating from the 2.8% growth in 11Q4. Service imports is forecast to grow by 0.3% and 1.5% in 12Q2 and 12Q3 respectively.

· Gross fixed capital formation surged by 12.2% in 12Q1, accelerated from the 9.8% growth in 11Q4. Infrastructural projects will continue to provide impetus for investment spending. The gross fixed capital formation is projected to grow by 3.2% in 12Q2 and 1.8% in 12Q3.

· Investment in land and construction went up by 2.0% in 12Q1. The infrastructural projects will continually provide growth momentum, with the growth rate projected to be 2.7% in 12Q2 and to 1.6% in 12Q3.

· Investment spending in machinery, equipment and computer software surged by 23.1% in the 12Q1. Underpinned by the low interest environment, investment in machinery, equipment and computer software is projected to increase by 3.6% in 12Q2 and 1.9% in 12Q3 when compared with the same period last year. The lower year-on-year growth rates are mainly due to a higher base of comparison.